After losing her Florida home to foreclosure in 2009, Sheila Ramos has made a home for her family on a patch of rural land on Hawaii's Big Island. (Paul Kiel/ProPublica)

Sheila Ramos' grandsons, 10 and 13, started crying. They wanted to know where the house was. There wasn't one. There was only a tent.

They had flown from Florida, after Ramos had fallen hopelessly behind on the mortgage for her three-bedroom home, to this family-owned patch of rural land on Hawaii's Big Island. There, on a July night in 2009, they pitched a tent and, with no electricity, started a new life.

If Ramos were in her 20s, living off the land might be a marvelous adventure. Hawaii is beautiful, and the weather is mild. In the nearly three years since she moved here, her family has built a semi-permanent tent encampment, and they now have electricity. But it's not how this 58-year-old grandmother, who has custody of her three grandchildren, imagined spending her retirement after working for more than 30 years — nine running her own businesses. She regularly scours the local dump and recycling center for items she can salvage.

The story of how she ended up in a tent is the story of how America ended up in a foreclosure crisis that has not ended, that still drags down the economy and threatens to force millions of families from their homes. Already, banks have foreclosed on more than 4 million homes since the crisis began in 2007. With almost 6 million loans still in danger of foreclosure, 2012 could very well be the worst year yet. Ramos' story is remarkable not because it's unique but because it isn't.

Her story doesn't fit any of the conventional narratives. Ramos is not a helpless victim. She made mistakes. But she didn't take out her mortgages to splurge on luxuries or build a new wing for her house. She took out her first mortgage to live the free-market dream of starting her own business. She took out later mortgages to cope with injuries sustained in a car accident.

Every step of the way, from her first subprime loan to foreclosure, her downfall was abetted by a mortgage industry so profit-driven and disconnected from homeowners that the common interests once linking lender and borrower have been severed. The lending arms of the nation's largest financial institutions helped plunge the country into crisis through their abuses and blunders, and they responded to that crisis with still more abuses and blunders — this time in how they handled people facing foreclosure. For subprime borrowers like Ramos, it has been as hard to work their way out of trouble as it was easy for them to get the loans that started their downfall. The millions of prime borrowers who thought they were doing everything right, only to be caught in a historic wave of unemployment, have been forced to endure a similar gauntlet of delays, errors and traps.

The industry developed tactics of dubious legality — not just robo-signing, which most Americans have heard of by now, but an array of business practices, some dating to the 1990s, that were designed to skirt the law and fatten profits. The federal and state governments largely tolerated these practices until they pushed Ramos into a tent and all of us into the Great Recession.

Even then, the federal government, facing an electorate bitterly divided over how and even whether to help "irresponsible" homeowners, responded in ways that proved ineffective. To be sure, the government's efforts were unprecedented, as Obama administration officials have repeatedly insisted. But those efforts were also halfhearted. Only recently, after the banks admitted to widespread law-breaking, did the government launch a response that might prove commensurate with the calamity.

This grandmother's story — outrageous and complex — is our story, the American foreclosure story.

Living the American dream

Born Sheila Ferguson, Ramos was one of seven children. The family lived in the small town of Haiku on the island of Maui, where her father did maintenance work at state parks. At 17, she married a man she'd met in high school, dropped out of school and had two sons, but divorced when she was just 19. She kept his surname, Ramos, but wanted a new life. Maui suddenly seemed small and confining, and she wanted "to get off the rock," as she puts it. So she took her two sons, aged 2 and 3, and left for Alaska.

She lived in Anchorage for three decades, building a life with her current partner, David Backus. After getting her GED and an associate's degree in cosmetology, she worked in various salons for several years, doing women's hair and giving facials. From there, she jumped to selling cosmetics in department stores, eventually working her way up to a managerial post at J.C. Penney — a role she loved. "I was a typical corporate diva," she says, always impeccably made up and dressed.

As the years rolled on — she worked at the company for nearly a decade — she gradually became disenchanted. When her brother died at 51, she decided "life was too short" to remain in a job she no longer enjoyed.

What came next was another reinvention. Her partner, Backus, was an electrician with a side business building large concrete vaults that house electrical equipment. Ramos began dabbling with the concrete, mixing and pouring it to make stepping stones for her garden, then planters for small trees. Soon she'd taken charge of the business and landed a contract to supply an Anchorage electric company with the utility vaults. Working in a small warehouse behind the Anchorage house she shared with Backus, she managed two employees as they mixed gravel, cement and water, poured the mixture into 1½-ton forms, and moved them to a truck to be delivered.

Ramos laughs when she recalls the amazement of friends and family at how she'd exchanged business suits and high heels for old sweatpants and rubber boots. "It broke my heart to give up those suits," she says, but jokes that she'd just traded slinging one type of mud for another.

She gained custody of her three young grandchildren after one of her sons and his wife were imprisoned on drug-related charges. Around the same time, her father had begun suffering from Alzheimer's, so her parents moved in. A friend, Elaine Shearer, remembers seeing Ramos working with concrete behind the house with a baby carrier on her back. Occasionally, when Ramos had to deliver her product at night, the children would join her, sleeping in car seats. Still, the job allowed her to set her own hours and stay close to home.

In 2004, her business took a major hit when another company underbid her and won the contract that had been her principal source of income for six years. Soon after, she packed up and decamped to Florida with her three grandchildren and her 83-year-old, recently widowed mother, ready for warmer weather and another reinvention. Backus remained behind but planned to rejoin the family once he retired.

On the Gulf Coast, about two hours north of Tampa, lies the community of Pine Ridge with well-kept, ranch-style homes, equestrian riding trails, a golf course, tennis courts and a community center. For less than $300,000, Ramos bought a 2-year-old house with 2,600 square feet and a swimming pool out back. Compared to Anchorage, it was paradise.

Using the proceeds from the sale of her parents' Hawaiian home, she was able to buy the house free and clear. No mortgage, no debt.

She wanted the freedom she had enjoyed working for herself. So, in the fall of 2004, she took out a mortgage on her new house for $90,000 and used the money to buy a local lawn-care business. First by herself and then working with one of her sons, she'd mow lawns, cut hedges and blow debris.

"I love to mow," she says. The business grew to about 40 customers, she recalls. "We were doing good."

"A little bit more to catch up"

In June 2005, Ramos was driving a few miles from the house with her mother and all three grandchildren. A car pulled out from a side road and crossed her lane. Traveling at 40-45 miles per hour, Ramos couldn't stop in time, and her minivan plowed into the other car. Ramos suffered a broken arm and injuries to her knee and hip. Her mother and granddaughter, then 10, injured their backs. Her car, little more than a year old, was wrecked. The police report puts the blame on the other driver, a woman who was 19 years old at the time and visiting from New Jersey.

In a single moment, Ramos had lost her car and ability to work. Customers dropped off one by one. Soon, the mortgage payment of $790 per month that had seemed well within her means became a burden. She began running up debt on her credit cards. About six months after the crash, she remembers, she fell behind by one mortgage payment.

Collection agencies began to hound Ramos. When Shearer visited her friend, "I would hear the calls coming in. It gets to a person after a while. I did see Sheila being worn down." The women had been friends for two decades, but "this was the first time where I heard her calling me and crying and saying, 'Elaine, I don't know where to go, I don't know what to do.'"

It was around the holidays, Ramos recalls, when a postcard came from Equity Trust Mortgage, proclaiming her eligible for another mortgage. She threw out that postcard, but the company ran classified ads at the time under the headline "REFINANCE NOW, LOW RATES" and promising, "Aggressive Programs: Fast Approvals, Fast Closings. Programs from good to poor credit. Non-income OK, limited credit OK. We can tailor a program for you. Call 24 hrs."

Ramos remembers thinking, "Maybe I'll just get a little bit more to catch up." She landed a $140,000 mortgage and paid off the $90,000 one she had used to launch her business.

Before moving to Florida, she'd never taken out a mortgage, she says, and was inclined to trust the mortgage broker, Stan Petersen, who ran Equity Trust Mortgage. He assured her it was OK, she recalls, and she didn't pay much attention to the details when she signed the paperwork.

After the old loan and numerous fees were paid off, the new loan brought her enough to buy a car and pay off her other debt but little else, she says. Then there was the monthly payment: It started at $1,150, more than the one on her last mortgage, which she hadn't been able to pay. She swore off credit cards. Still, she says, the new mortgage left her "just surviving."

It was a subprime loan, so the worst was yet to come. After two years, the initial fixed interest rate of 9.25 percent would switch to an adjustable rate. It could never dip below the initial rate but might rise as high as 14.25 percent. If Ramos attempted to escape the loan by refinancing or selling the house before the rate hike, she'd be liable for a penalty of about $5,000.

Around this time, one of her sons wanted to live on his own. So, five months after getting her new mortgage, Ramos took out another $28,000 loan against her home to purchase a trailer for him. It didn't add to her expenses because her son made the monthly payments.

But Ramos was doing what so many Americans did at that time: using her home as an ATM as the frenzied buying of the bubble years raised the value of nearly every house in the country. From 2004-06, American homeowners extracted nearly $1.5 trillion out of their homes, providing a huge boost to the economy. While a lot of that money went to general consumer spending, particularly home improvements, the largest amount went to pay off other debt. Ramos was typical in using the money from her various mortgages to keep her head above water. Many also used the funds, as she'd done, to start a business.

At this time, she, her mother and granddaughter were still being treated for their injuries. She'd hired a lawyer to pursue a settlement with the other driver's insurance company, but that was dragging on. After working for more than 30 years, she was convinced it would be just a little bit longer before she was healthy and back at her business. Instead, she began falling behind on her payments again.

To stay afloat, Ramos borrowed from friends and relatives, which weighed on her, her friend Shearer says. "She was never one to owe anybody anything before."

Ramos would get occasional calls from Petersen, her mortgage broker. "He was like my best friend," she recalls. "He'd say, 'Hi, Sheila, how are you doing?'" He knew about the car accident and that she was struggling, she says. But when she asked whether she should just put her house up for sale, she recalls, he said there was no need because she could get yet another loan, one that would allow her to pay off her current ones plus give her some money to make the first payments on the new loan. That would tide her over until she got the accident settlement and could work again. "We'll send an appraiser out, and we'll get you this loan," she remembers Petersen saying. "‘You've got plenty of equity, don't worry.'"

The three-bedroom home in Florida that Ramos lost to foreclosure. (Paul Kiel/ProPublica)

Less than a year after her first big refinance, her second major loan was much larger: $262,000. Her home, however, had been appraised at $403,000, which, if true, meant that it was gaining about $40,000 in value every year. Seen that way, the loan seemed almost conservative.

As with all her other dealings with Petersen, she recalls, he himself did not appear; instead, a woman came in the evening with a stack of papers. Ramos remembers that the woman was running late and hurriedly prompted Ramos to initial or sign her way through. The whole whirlwind ceremony at her kitchen table, she says, took about 15 minutes.

The new loan was also an adjustable rate mortgage, and her initial monthly payment was about $2,200 per month, nearly triple that of her first mortgage.

To make those payments, she recalls, Petersen had told her she could use the proceeds from the refinance. After paying off her two previous mortgages, the penalties for paying them off early and various loan fees, she would receive $65,000 in cash.

As Christmas approached, the money had yet to arrive. On Dec. 19, Ramos overdrew her checking account twice when she made two debit-card purchases — for $9.09 and $7.50 — at a Winn-Dixie supermarket. The two overdraft fees came to $66. The next day, a $37.50 check and a $35.66 charge at Kmart cost her $66 more in overdraft fees. A day later, a $9.95 purchase brought another $33 overdraft fee.

But that day — Dec. 22 — the $65,000 finally landed in her checking account, and it was a new day.

She repaid friends and relatives from whom she'd borrowed thousands. Her bank records show she caught up on her taxes, her cable, internet and utility bills. She got her car fixed. She bought Christmas presents. She took her grandchildren to a resort near Disney World "to give them a treat because they'd been so stressed," she recalls.

Within two months, about $30,000 was gone. Looking back today, she can't remember where it all went: "It seems like a dream."

The Wall Street mortgage machine

Ramos signed the papers for her $262,000 mortgage in December 2006. She didn't know it, but she was riding the last wave of the subprime boom.

Arranged by her local broker, Petersen, the loan was made by a nationwide subprime lender called Mortgage Lenders Network USA. Months earlier, the company, then the nation's 15th-largest subprime lender, had broken ground on a $100 million, 300,000-square-foot headquarters building in Connecticut. But less than two weeks after issuing Ramos' loan, the company stopped funding new ones. It soon furloughed employees. By February 2007, it had declared bankruptcy.

Before it collapsed, Mortgage Lenders Network sold Ramos' loan to Wall Street. The buyer was Merrill Lynch, which bundled it with 6,282 other mortgages totaling $1.4 billion and packaged them into a security, the "Merrill Lynch Mortgage Investors Trust, 2007-MLN1." Investors were invited to buy different classes of the security, arranged from least to most risk. Most of the mortgage loans, like Ramos', had been made to borrowers with poor credit histories. Nevertheless, the credit-rating agencies Moody's and Standard & Poor's gave AAA ratings to the security's safest classes, meaning they were supposedly investments of the "highest quality, with minimal credit risk."

The 326-page offering document does include warnings. On page 17 it says, "In recent months, delinquencies and losses with respect to residential mortgage loans generally have increased and may continue to increase, particularly in the subprime sector." What's more, most of the loans, like Ramos', had adjustable rates that might jump after two years, which could lead to more defaults and foreclosures. Also, a decline in housing prices could make it impossible for borrowers to sell their homes or refinance, trapping them in foreclosure. And most of the loans went to people with poor credit.

It goes on. Many subprime lenders like Mortgage Lenders Network were struggling or failing because their loans were performing so poorly. They were also being accused of fraud, the document says, though it just notes the general trend and doesn't say that Mortgage Lenders Network faced that charge.

Despite those caveats, the document asserted that the loans in the pool had been made according to reliable underwriting guidelines, meaning the borrowers' history, assets and income had been carefully reviewed by Mortgage Lenders Network. "The consumer's ability to pay is of primary importance when evaluating applications," it said. Still, Merrill Lynch could not "provide any assurance that MLN had followed the stated guidelines with respect to the origination of any of the Mortgage Loans."

The security found buyers, including the government-backed mortgage behemoths Fannie Mae and Freddie Mac. In a federal lawsuit filed in September 2011 against Merrill Lynch, the federal agency overseeing Fannie and Freddie claimed the companies were swindled when they purchased the pool that included Ramos' loan (and 87 other securities sold from 2005-07). Merrill has denied wrongdoing.

As in dozens of other cases filed in recent years by investors in subprime securities — often pension funds that were looking for safe, AAA-rated investments — the suit argues that the mortgages were worse than the offering documents represented them to be, leading to large losses.

According to the complaint, the appraisers, working with lenders and brokers, inflated the value of homes. In the case of Ramos' pool, the suit claims that more than a quarter of the loans exceeded the value of the homes, while the offering had said that none did. The offering also misrepresented the number of properties that were actually investments, not primary residences, the suit says. Those are seen as riskier loans because the borrower is likelier to abandon the property.

Then there's the issue of how much money the borrowers were making. While subprime loans were by definition given to people with poor credit histories, those borrowers were supposed to have sufficient income to make their payments. But, the suit charges, many didn't. Lenders and brokers often failed to verify the borrower's income or just made it up.

Sheila Ramos' loan was arranged by Petersen, her broker. Mortgage brokers were the ground troops for the subprime boom. More than 200,000 people began work as mortgage brokers during the boom, according to the Financial Crisis Inquiry Commission's report. Not only did they steer a borrower to a certain lender, they typically prepared the paperwork for the loan. They often purported to be acting in the best interests of the borrower, but they had a financial incentive to steer their customers to more expensive loans. Their compensation was often tied to the interest rate; the higher the interest rate, the more they were paid.

And they had no long-term stake in the loan: "For brokers, compensation generally came as up-front fees," states the FCIC report. "So the loan's performance mattered little."

Fraud was widespread in the industry.

Petersen's company had a big payday for originating Ramos' loan, according to the loan documents. From Ramos, the company received $8,200 in fees just for setting up the loan. But Petersen also got $5,238 from Mortgage Lenders Network for originating a high-interest-rate loan. The company collected a total of $13,438.

Petersen's haul was big even for the boom years. Back then, brokers commonly earned about $10,000 for subprime loans the size of Ramos', says Fred Arnold, a director of the National Association of Mortgage Professionals. Rules enacted since the housing crash — particularly by the Federal Reserve — have since restricted how brokers are paid.

Ramos says she clearly explained her situation to Petersen: that she wasn't working because of her injuries and that her family was making do with her mother's Social Security payments and what little other income they could muster. Petersen had the opportunity to verify her meager earnings. The mortgage file, reviewed by ProPublica, includes an authorization form allowing Petersen to examine Ramos' bank statements and tax returns.

Fifteen months later, when she was facing foreclosure, Ramos began to investigate the facts of her loan. She requested her loan documentation from Petersen's office, which provided it. She says she was shocked to find that her loan application listed her income as $6,500 per month.

The application, reviewed by ProPublica, includes other inaccuracies. It lists her as actively self-employed, but her business had fallen apart by that point. It also states that she was not currently delinquent on any mortgage even though Petersen's company, according to the loan file, had reviewed documentation showing that she was.

She called Petersen, she says, and asked why he'd falsified her income. She recalls his answer: "‘Well, you got your loan, didn't you?'"

It was "extraordinarily common" for homeowners who took out mortgages during the boom to be later surprised by what their mortgage brokers had put on their loan applications, says Robert Bridges, a former mortgage loan auditor. His job was to check mortgage files and call homeowners who'd fallen behind on their mortgages to see whether there were any misrepresentations on the loan application. Over the past several years, he's investigated thousands of cases on behalf of mortgage insurance companies that wanted to make sure they didn't pay out on any improperly issued loans. Often, Bridges says, he'd tell a homeowner how much income the loan application said they were making. "They'd go, ‘What? Where'd you get that number? If I made that much money, I wouldn't be in this situation.'"

After Ramos found that her income had been misstated, she complained to everyone she could think of. She sent letters and emails to the FBI, the Florida governor's office and the state's Office of Financial Regulation. "My stated income was falsified and none of the information I gave him was confirmed," said her 2008 letter to the FBI Mortgage Fraud Division. Then, echoing what Bridges said he had heard from so many homeowners, Ramos wrote: "He stated my income at 6,500 per month. If I had this I would not need a loan."

Reached on his cell phone, Petersen declined to comment, saying only that "the company's closed." He has not been charged with a crime.

Neither Mortgage Lenders Network nor any of its executives have been charged with a crime, either. But in an unusual court filing, federal prosecutors have confirmed the company's practices are under investigation. In early 2011, the trustee overseeing the liquidation of the company proposed, as a cost-saving measure, destroying a warehouse full of mortgage files. The Justice Department objected, arguing that the files shouldn't be destroyed until investigators had had a chance to thoroughly review them. The company's "loans are the subject of many ongoing investigations," said the submission to the bankruptcy court. Representatives for the defunct company declined to comment.

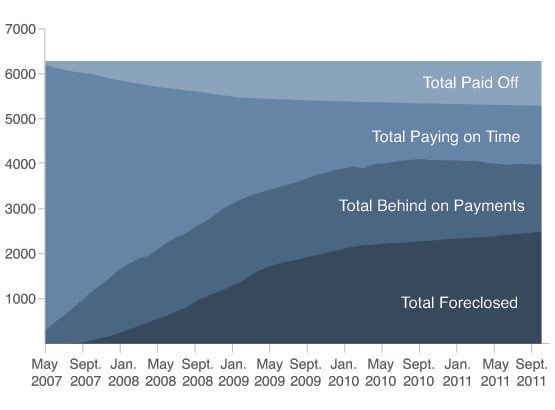

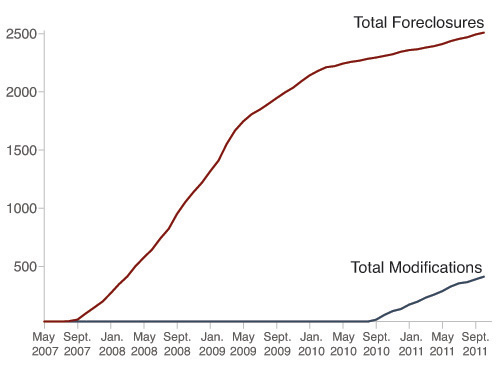

The mortgages bundled into "Merrill Lynch Mortgage Investors Trust, 2007-MLN1" have not fared well. As of October 2011, about 40 percent of them had been foreclosed on, as shown in the chart below, taken from investor reports. Another 21 percent of the borrowers are behind on their payments and facing foreclosure.

How Homeowners Are Faring

in the Security that Includes Ramos' Mortgage

Sources: Deutsche Bank trust reports, ProPublica analysis

Moody's and S&P now rate the safest classes of the security — once judged as having "minimal" risk — as having "very high" risk. It's a junk bond.

Similar securities have also fared poorly. Among the 88 Merrill Lynch securities targeted by the Fannie Mae and Freddie Mac lawsuit, all have high rates of foreclosure and delinquency. When the suit was filed last fall, on average, a little more than half of the homeowners had either already lost their homes to foreclosure or were in danger of doing so.

The collapse of hundreds of securities like these precipitated the 2008 financial crisis and plunged America into the Great Recession.

The mortgage servicing industry

One day in the mail, Ramos received a notice that she had missed a mortgage payment. The notice came from a company she'd never heard of, Wilshire Credit Corp. "I was confused," she says, because she'd sent her payments to her lender, Mortgage Lenders Network. Why was this other company, Wilshire, suddenly asking her for payments?

In a bygone era, the bank that made the loan held onto it and collected the payments. In today's system, that's rare. Instead, the job of actually dealing with homeowners and collecting loan payments falls to mortgage servicers.

Serving homeowners is decidedly not the mortgage-servicing industry's focus. Servicers rarely have a stake in the loan itself. They are middlemen, collecting payments from homeowners, keeping a small cut and passing the bulk to investors. They make money keeping costs low. Hiring employees to speak to borrowers about avoiding foreclosure, for example, increases costs and diminishes profits. So, in general, servicers make money by providing as little service to homeowners as possible.

During the housing boom, the industry underwent a dramatic consolidation. In 2004, the 10 largest servicers handled about a quarter of the country's mortgages. By late 2008, the five largest handled about 60 percent. It was a high-volume, low-cost business that boiled down to processing payments. Interaction with the customer was minimal and, when it did occur, involved call-center employees who often made as little as $10 per hour.

That model hummed as long as relatively few people fell behind on their mortgages. With the housing crash and ensuing recession, everything changed. Delinquent homeowners stopped sending their monthly checks, so instead of processing payments that had come in like clockwork, servicers suddenly had to shoulder the much more expensive tasks of making collection calls, considering the homeowner for some sort of modification or payment plan, and seeking foreclosure if the homeowner fell far enough behind.

Servicers were unprepared. Their employees lacked sufficient training, and there were too few of them. They lacked proper equipment and relied on outdated computer systems. And there was little financial incentive to spend time working with customers. Handling a delinquent loan costs the servicer more than 10 times as much as a loan on which the borrower is making the monthly payments, according to an estimate by federal regulators.

Just as Ramos didn't know that Merrill Lynch had bought her loan and then sold it to investors, she also didn't know that Merrill Lynch had selected its own subsidiary, Wilshire, to collect her payments. A small servicer based in Beaverton, Ore., with about 800 employees at the time, Wilshire specialized in handling subprime loans.

In the offering documents for the security that included Ramos' mortgage, Merrill Lynch assured investors that homeowners would be in good hands. Wilshire had ample experience with borrowers who were "experiencing financial difficulties." Their employees were hands-on, prepared for "substantial personal interaction with the obligors to encourage them to make their payments timely, to work with them on missed payments, and to structure individual solutions for delinquent obligors."

Typical for mortgage servicers, those phone calls would come from the company's collections department. At the same time, homeowners would hear via letters and phone calls from Wilshire's "loss mitigation" team, which was charged with deciding whether to foreclose or pursue a "viable workout opportunity." The offering documents give little detail on how foreclosure might be avoided. However, the company said it would be quick in deciding to foreclose if necessary.

Ramos, of course, had taken out the loan because she was "experiencing financial difficulties." The loan had bought her time, but how much? She was still injured and unemployed, leaving next to no income for the household, which was now saddled with a $2,200 monthly mortgage payment. Her checking account went one way: down, month after month. By the middle of 2007, little more than half a year after the $65,000 had landed in her checking account, the money was gone.

Nevertheless, she had hope. She'd taken in an elderly family friend with Parkinson's disease to take care of alongside her mother, and his Social Security payments provided a little additional income. One of her brothers had also moved in after discovering he had leukemia. He agreed to help with the payments while he underwent treatment. She started housecleaning because, even with her weak left arm, she could do that work: She and her teenage granddaughter labored together for the few clients she was able to find. Altogether, she figured, it might be enough to make the mortgage and get by. Her lawyers also had finally launched a suit over the car accident, and she was hopeful they'd win some extra damages beyond paying for her treatments.

But she was continually falling behind and catching up, a pattern that began even before the loan funds had run out. She says she often thought she'd made a timely payment only to find that Wilshire considered it overdue. Late charges and other fees made her climb steeper. The company's employees often called and pressed her to make her payments, but she says no one could clearly explain the reason for certain charges or what she needed to do to catch up.

Ramos had entered the maddening, Kafkaesque maze of dealing with servicers. Her complaints echo those of consumer advocates and tens of thousands of borrowers who say servicers routinely lost documents, didn't answer questions, kept homeowners on endless hold or transferred them to people who knew nothing about their situations. Indeed,servicer errors have often made bad situations worse, sometimes even pushing borrowers into foreclosure. The accounting problems have been exposed in bankruptcy proceedings, which can force servicers to disclose exactly how they handled loans. Bankruptcy judges, who sometimes get so angry they scold servicers from the bench, have penalized companies for improperly processing payments, attempting to collect money they're not owed and charging unwarranted fees.

"Everyone gave me the runaround," Ramos recalls. When she tried to get answers, she often found herself being transferred to this or that person, only to end up leaving a voice-mail message for someone she knew wouldn't call her back.

"You just don't understand how hard she worked at this," says Shearer, her friend, who recalls watching Ramos spend hours on the phone. "Nobody knew anything, and they'd pass you from one person to the next. It just seemed like she never could get the horse by the tail."

After nearly a full year of falling behind and catching up, Ramos tried to make a payment in March 2008, but Wilshire refused it. At the time, she was less than a month behind, according to payment records kept for investors in the security. But Ramos remembers being told that she was too far behind on her payments to make any more and that she should expect to hear from another Wilshire employee about what would happen next. Ramos had reached the brink of foreclosure. She reached out for help from housing counseling nonprofits. "My loan company will not work with me Please Please help me save our home," she wrote to one.

A win-win

Ramos was part of a growing wave of defaults. Housing prices had been tumbling for more than a year after peaking in 2006, meaning that many delinquent borrowers could no longer sell their homes to get out from under their debt, because their homes were now worth less than they owed. For a subprime servicer like Wilshire, the downturn meant that nearly half of the subprime loans it handled were delinquent.

That was a problem for lenders, for the Wall Street banks that had bought such loans, for the investors who'd purchased securities Wall Street concocted out of these loans, and, of course, for borrowers who were losing their homes, their savings and their creditworthiness. For policymakers, the solution was clear: Get struggling homeowners into affordable loan modifications.

To be sure, modifying a loan by reducing the interest rate, for instance, would mean a loss — or lower profit — for the investor. But if foreclosure was likely to result in even higher losses, then a modification was preferable. Given plummeting home values, a modification would often save the investor money. It seemed like the ultimate win-win.

The earliest governmental program had a modest aim: to make sure the servicer merely considered a modification before pursuing foreclosure. In October 2007, President George W. Bush's administration launched the Hope Now Alliance to provide a forum for servicers and housing counselors to communicate.

"The first step to avoid a foreclosure was for the servicer and borrower to talk to one another," wrote former Treasury official Phillip Swagel in a 2009 narrative of the financial crisis, "but this was not happening in a surprisingly high proportion of instances — some estimates were that half of foreclosures started without contact between borrower and lender or servicer."

So, at the administration's prompting, servicers backed the launch of a hotline (888-995-HOPE) that homeowners could call to speak with a housing counselor, and the companies agreed to send notices to delinquent borrowers about it. President Bush himself recorded a public service announcement encouraging homeowners to call.

But even if a homeowner contacted a counselor and qualified for a modification, there was no requirement that the servicer offer one. In fact, there were no requirements at all for servicers. The alliance was administered by the Financial Services Roundtable, a powerful banking industry trade group and headquartered in its offices.

Loan modifications were indeed a win-win for everyone — except the servicers. And it was the servicers who were the deciders. They determined whether homeowners like Ramos got loan modifications.

Servicers earn their main revenue through a small fee for handling each loan, usually between .25 and .5 percent of the principal each year, depending on the type. (Riskier loans like Ramos' netted more.) But servicers have another big income stream: penalty fees and foreclosure-related charges.

Ramos' case shows how lucrative such fees could be. If Ramos had made all of her payments on time, Wilshire would have received only about $1,300 (.5 percent of her outstanding principal) in the first year of handling her loan. But if Ramos was more than 10 days late with a payment, it generated a late charge of 10 percent of the overdue payment — in her case, about $220. That amount would then be due on top of what she owed.

Experts say these terms were especially punitive even for subprime loans, which typically gave borrowers more time and penalized them less for being late. While Ramos no longer has records showing how much she paid in late fees, an August 2008 breakdown by Wilshire of unpaid charges on her account shows outstanding late fees of $770 and a returned check charge of $50 — an extra $820 on top of its base of $1,300.

Ramos shows a breakdown by Wilshire of unpaid charges, including outstanding late fees of $770 and a returned check charge of $50. (Paul Kiel/ProPublica)

If Ramos or other troubled homeowners could somehow scrape together the money to pay such fees, great. But the true genius of the business model is that it didn't matter whether borrowers could pay the fees. If a homeowner went bust and the house was sold through foreclosure, no problem. The securitization contracts ensured the servicer was first in line to collect.

It was a virtually fail-safe income stream. In 2008, Ocwen, a subprime servicer similar to Wilshire, received about 19 percent of its mortgage-servicing income from such fees. In fact, some servicing executives assured analysts that mounting delinquencies would actually help their companies.

David Sambol, chief operating officer for Countrywide, then the country's largest subprime lender and servicer, pitched this idea to stock analysts during a fall 2007 earnings call. His company, he claimed, would benefit from "greater fee income from items like late charges" and the company's "counter-cyclical diversification strategy" of running businesses involved in foreclosing on homes, such as property inspection services. As more and more homeowners ran into trouble and then foreclosure, the servicer could count on more short-term income, not less.

In 2010, the Federal Trade Commission sued Countrywide, accusing it of a widespread scheme to profit from delinquencies and foreclosures by hitting homeowners with bogus or marked-up charges. Countrywide settled the suit without admitting any wrongdoing. It agreed to stop overcharging borrowers and pay $108 million to consumers who'd been affected.

Compared to Countrywide, Wilshire was tiny and hasn't been charged with wrongdoing. But the larger economics were the same: If Ramos kept paying, Wilshire made money. If she lost her home, Wilshire made money.

The one option that didn't make financial sense for servicers was spending money on staff and equipment to make sure that homeowners like Ramos were adequately reviewed for modifications. Trained employees would have to spend valuable time analyzing the borrower's situation and, in effect, re-underwrite the loan. Worrying too much about unnecessary foreclosures would cut into servicers' profits. Servicers also worried that investors might object to cutting homeowners' payments and sue to recoup any supposed losses. No forum for servicers and borrowers to "talk to one another" was going to change the fundamentals of the servicing industry: Collect payments or foreclose.

In the rare event that a homeowner did receive a modification, it didn't typically lower the homeowner's payments, according to a 2008 report by federal banking regulators. About a third of the modifications granted in 2008 actually made the payments go up, because all the servicer had done was lump the arrears and fees into the principal and then amortized the new, higher balance over the life of the loan. About a quarter of the time, the payments stayed the same, and only about 42 percent of the time did they actually go down. As a result, most modifications merely delayed foreclosure. By the end of 2009, according to regulators, more than two-thirds of the homeowners who'd received modifications in 2008 had fallen behind again.

In 2008, Merrill Lynch, Wilshire's corporate parent, reacted to the downturn not by expanding but by freezing hiring at Wilshire. No new staff was added, and departing employees were replaced by temp workers, many of whom had scant experience in the mortgage industry. For Merrill, the logic was clear: The bubble had popped; investors were no longer willing to buy packages of subprime loans, so there would be few if any new loans for Wilshire to handle. So what if most of the old loans would now require far more time and effort? Wilshire would just have to make do with the staff it had.

"Dear Valued Customer"

It was through the HOPE Now hotline that Ramos found a housing counselor with Consumer Credit Counseling Service, a large Atlanta-based nonprofit that has since changed its name to CredAbility. She went through all her income and expense information, and the resulting worksheet, prepared by the counselor, shows Ramos with monthly income of $4,700, which was enough to cover her regular monthly mortgage payments (not including fees) as well as her living expenses with about $300 left over.

The counselor told her she was a good candidate for a mortgage modification, meaning that it would not only help Ramos but be in the best financial interest of the investors. Here was a case of that win-win. With home prices plummeting, kicking Ramos out of her home meant a certain loss for investors. Even a generous modification would likely cost them less. All that was required was for the servicer to put its own interests — maximizing fees and minimizing costs — to the side.

Studies have shown that homeowners working with counselors have fared better than those working on their own (a low bar to clear), but counselors have often complained that they spent a lot of their time just trying to get homeowners' applications acknowledged and reviewed. Delays and lost documents have been the rule.

So it went with Ramos and her counselor: Their major hurdles were logistical — getting someone, anyone from Wilshire on the phone and getting that person to acknowledge receipt of documents that they had sent to the company. Ramos' counselor sent the same documents several times, Ramos remembers. Even though Wilshire was a member of the HOPE Now Alliance, Ramos remembers a Wilshire employee telling her that there was no need to go through a counselor: She could simply contact the company directly — which, of course, she'd had no luck doing.

Ramos knew she couldn't rely on Wilshire for help. In the months that passed while she waited for an answer to her application for a modification, she looked for other options. She listed the home for sale with the help of a friend who offered to waive her commission if it sold, but there were no takers. She began searching for a homeless shelter in the area that could take all seven people in the house if they were suddenly evicted, but found that no shelter could.

She got help from neighbors. One day, during one of her many conversations with Wilshire employees, she recalls that an employee told her the company might allow her to resume making payments if she made a lump-sum payment of around $5,000. She told one neighbor, Dave Shea, about the offer, and Shea decided to make the rounds in the neighborhood asking for donations.

"I knocked on a lot of doors," Shea said. "I know a lot of folks."

He told them their neighbor was facing foreclosure and needed help getting caught up. One by one, they handed over $50, $100, sometimes several hundred dollars. It wasn't a hard sell, he says. "These people are just willing to help."

Eventually, he delivered about $5,000 to Ramos. Elated, she went with her brother to his credit union to deposit the money and convert it into a cashier's check, she recalls. Wilshire, as do many servicers with delinquent homeowners, required payment with guaranteed funds. They mailed it off, hopeful they'd finally stopped the snowballing growth of her debt, she says. But where those funds went — whether they were deposited and not applied to her mortgage or simply lost — she still doesn't know. How servicers handle payments is often a mystery to homeowners, who often complain that they're lost or misapplied.

On July 12, 2008, Ramos got her first clear response to her efforts to catch up: a summons. "A lawsuit has been filed against you," it said. Wilshire had decided to foreclose.

Ramos' chances for a modification at Wilshire, it turns out, were dismal. In 2009, as part of a report on Wilshire's servicing performance, the credit-rating agency Fitch analyzed how people in Ramos' situation — subprime borrowers who were delinquent in early 2008 — had fared. A year later, only about 12 percent had either caught up on their payments or managed to pay off their loans (mostly through selling or refinancing). The rest — fully 88 percent — had already lost their homes, were in the foreclosure pipeline, or were still behind and likely destined for foreclosure.

Bank of America spokesman Rick Simon, speaking for Wilshire because the bank later acquired the company, says the servicer had reviewed Ramos numerous times for some sort of foreclosure alternative. Back in February or March 2008, there had been "a discussion of setting up a formal six-month payment plan," he says, but Ramos hadn't agreed. Ramos has no memory of such a conversation.

The payment plan was Wilshire's preferred solution to delinquency in 2008, according to a Moody's report, and a favorite industry tool: The servicer simply tacked missed payments and fees onto regular payments. The result, of course, was even higher payments for the struggling borrower.

Three months later, in June, Simon says, Wilshire declined Ramos' application for a modification. The company then reviewed her for another payment plan but rejected that, too. Simon declined to provide the reasons for the denials or evidence that Ramos had been notified. Ramos, for her part, doesn't remember ever hearing about any of this before she was sued.

Instead, almost a week after Wilshire launched a foreclosure suit, it sent her a letter, which read in full:

Dear Valued Customer:

In connection with the above referenced loan, Wilshire Credit Corporation ("Wilshire") has reviewed your request for a MODIFICATION. Please be advised that after careful consideration, Wilshire has declined to approve your request.

If you have any questions, please contact us at our toll-free number above.

Sincerely,

Loan Workout

The bailout

It was in 2008 that the full force of the foreclosure crisis hit. Housing prices went into free fall — by year's end, Tampa home prices had tumbled about a third from their peak. Foreclosures skyrocketed, rising about 80 percent from 2007. In September, the investment bank Lehman Brothers went bankrupt, and the beating heart of the financial system seized up.

"I felt that this is something like I've never seen before, and the American public and Congress don't fully understand the gravity" of the crisis, legendary investor Warren Buffett recalled in a 2009 interview with The Wall Street Journal. "I thought, we are really looking into the abyss."

Ramos reviews a court document. (Paul Kiel/ProPublica)

Though the crisis had spread far beyond real estate, mortgages like Ramos' — bundled, sold, bundled again, insured and insured against — were the absolute epicenter. Banks and insurance companies carried billions of dollars of mortgage-related assets on their balance sheets, and those assets were plunging in value by the day. Yet, HOPE Now, with its goal of encouraging homeowners and servicers merely to communicate, was still the government's chief effort to stem the damage.

For reformers, the near collapse of the financial system and the ascension of an energetic new president whose party controlled both houses of Congress provided an opportunity to act boldly. Until that point, the idea of using taxpayer dollars to stem foreclosures — supported by some Democrats and economists in the Bush administration's Treasury Department — had been a political nonstarter because of the perception that it would reward irresponsible behavior. But in October, Congress passed legislation creating the $700 billion Troubled Asset Relief Program, more commonly known as TARP or simply "the bailout."

The TARP plan, formulated by Bush's Treasury Department, was for the government to buy up the "troubled assets," mainly those securities backed by mortgages that were defaulting in droves. Democrats agreed but pushed for a clause that would mandate the government to modify the loans contained in the assets it purchased. With the government as the dominant owner of the assets, the thinking went, it would be in a position to dictate how they were handled. After the bill passed, the stage seemed set for the government to rescue not only the country's largest financial institutions but also millions of homeowners.

Less than a month after the bill passed, Treasury Secretary Hank Paulson changed course. Buying up the assets would be too complicated and take too long, he decided. The financial system needed quicker intervention. So, the Treasury Department invested directly in the banks. Along with the billions being loaned daily by the Federal Reserve, the move stopped the economy's free fall. But it did nothing to address foreclosures.

Obama's options

In the wake of that decision, two broad alternatives emerged.

Federal Deposit Insurance Corp. Chairman Sheila Bair, appointed by Bush, had been agitating since at least 2007 for modifications. Now, she proposed a system of incentivesto make affordable modifications more attractive to servicers and investors. Using a $24 billion pool of TARP funds, the FDIC would pay servicers $1,000 for each modification. That money would help offset the costs of evaluating the borrower and compensate the servicer for forsaking the quick returns from foreclosure. The FDIC would also provide insurance on any modified loans by sharing the loss if the homeowner defaulted again and ended up in foreclosure. For investors, Bair thought, modifying loans through the program would be a no-brainer, and they would lean hard on servicers to push them through. Many Democrats supported the idea.

If the FDIC plan was about dangling carrots, the other option was all stick. Called "cramdown," it relied on bankruptcy courts to force a modification on investors and servicers.

Current law allowed judges to slash credit-card and other kinds of debt (even mortgages on second homes), but the debtor's primary mortgage on a principal residence was off limits. That's why Ramos hadn't declared bankruptcy. She didn't have much debt outside of her mortgage, so at most, declaring bankruptcy might have slightly delayed her foreclosure.

But if the law were changed, then bankruptcy might have made sense for Ramos. A bankruptcy judge would have assessed her financial situation and the true market value of her home. If the judge found Ramos had enough income to keep the home, then he could cram down her debt by reducing the interest rate, the principal, or both.

In fact, the carrot of incentives and the stick of forced modifications probably worked best together: The threat of a bankruptcy judge stepping in would provoke servicers to modify loans. "That was always the thought, that judicial modifications would make voluntary modifications work," says North Carolina Rep. Brad Miller, one of several Democrats who were pushing cramdown legislation.

Republicans and the banks vehemently opposed cramdown. "It undermines the foundation of the capitalist economy," says Swagel, the former Bush Treasury official. "What separates us from [Russian leader Vladimir] Putin is not retroactively changing contracts."

Banks, of course, didn't want a third party slashing their loans and potentially costing them billions in lost interest and write-downs. "Every now and again an issue comes along that we believe would so fundamentally undermine the nature of the financial system that we have to take major efforts to oppose, and this is one of them," Floyd Stoner, the head lobbyist for the American Bankers Association, told an industry magazine.

Democrats tried and failed to include cramdown in the TARP legislation, in part because then-presidential candidate Barack Obama, who was leading in the polls and was consulted by Congressional leaders, thought something so controversial might "cloud this thing with partisan politics," as he put it, and imperil the bill's passage.

But cramdown's backers remained optimistic. After all, Obama had campaigned on it and, shortly after rejecting the idea of including it in the TARP, had called it "the right thing to do, to change our bankruptcy laws so that people have a better chance of staying in their homes." He promised Democrats he'd "push hard to get cramdown into the law," Miller recalls.

Cramdown would change the law, requiring an act of Congress. But Sheila Bair's incentives could be enacted unilaterally by the executive branch.

Less than a month into his presidency, Obama announced his new plan. "In the end, all of us are paying a price for this home mortgage crisis," he told a cheering crowd in Mesa, Ariz. "And all of us will pay an even steeper price if we allow this crisis to continue to deepen — a crisis which is unraveling homeownership, the middle class and the American dream itself. But if we act boldly and swiftly to arrest this downward spiral, then every American will benefit." The program, he promised, would "enable as many as 3 to 4 million homeowners to modify the terms of their mortgages."

Even as he spoke, Treasury Department officials were still scrambling to work out the details — rules and calculations that would bear enormous consequences for millions of homeowners like Ramos and for the American economy. "We didn't have much on paper at that time," Laurie Maggiano, policy director for the new program, would later say.

In the end, the Home Affordable Modification Program, or HAMP, plucked a few ideas from Bair's carrot approach: For example, servicers would receive $1,000 immediately upon granting a modification to erase their incentive to foreclose and compensate them for evaluating homeowners' ability to afford the modified loan. That incentive was not based on hard evidence. "It was just a guess that $1,000 might be enough," says Karen Dynan, a former senior economist at the Federal Reserve.

But the administration's final plan lacked an incentive Bair considered crucial: having the government bear half the loss of any modification that failed. The administration balked. To have taxpayers eat the losses caused by deadbeat borrowers was seen as political dynamite. A Gallup poll taken in the fall of 2008, for example, had found that 79 percent of Americans cited "people taking on too much debt" as the main cause of the financial crisis. ("Banks making risky loans" was second, at 72 percent.) Instead, Treasury designed the system to pay investors for modifications, but only in increments and only if the borrower continued to make payments. The program only "paid for success," the administration boasted. On average, investors could hope to reap about $15,000 in subsidies over five years.

Bair saw another flaw she considered fatal. "In addition to the lack of economic incentives," she later explained, "the operational complexity was mind-boggling. The big servicers do not pay or train their staff as well as they should. The turnover is very high. That's the reality. You really have to make it simple for the program to be operationally effective."

In her view, the carrot needed to be juicy, sweet and easy to get — because there were no penalties. Servicers didn't have to participate at all; if they volunteered for the program, they signed a contract with the Treasury Department agreeing to follow the rules in return for the incentives.

In the view of many on the left, the program put the government in a weak, almost supine position. But that was still too much for some on the right, who attacked the plan as a bailout for "losers."

The day after Obama announced the creation of HAMP to that cheering crowd in Arizona, CNBC commentator Rick Santelli excoriated the program in a rant that is widely credited as sparking the Tea Party movement, which jolted American politics to the right. "How many of you people want to pay for your neighbor's mortgage that has an extra bathroom and can't pay their bills?" Santelli thundered. Do Americans, he asked, "really want to subsidize the losers' mortgages"?

Cramdown's proponents saw HAMP as merely a first step. Publicly, the administration still supported cramdown, but its supporters saw worrying signs. The White House "kept punting" when Democrats pushed for cramdown to be attached to larger pieces of legislation such as the stimulus bill, says former Rep. Jim Marshall, a moderate Democrat from Georgia and cramdown backer. In private meetings, Treasury staffers began conversations with congressional aides by saying the administration supported cramdown and would then "follow up with a whole bunch of reasons" why it wasn't a good idea, says an aide to a senior Democratic senator.

The administration feared the consequences for the nation's biggest banks, which had been rescued just months earlier. If too many consumers were lured into bankruptcy, they wouldn't have only their mortgages reduced. They might very well have other debts slashed, such as home-equity loans and credit-card debt. The cumulative effect could devastate the banks, plunging the nation back into a financial crisis.

Cramdown's Democratic supporters needed the president's vigorous support, because the measure faced powerful opponents: not just the too-big-to-fail banks but small banks and credit unions. "The community banks went bonkers on this issue," says former Sen. Chris Dodd, D-Conn., then head of the Senate banking committee. Democratic leaders offered to exempt smaller banks from the legislation but couldn't reach a deal. After narrowly passing the Democrat-controlled House, cramdown was defeated in the Senate when 12 Democrats joined Republicans to vote against it.

Some like Rep. Barney Frank, D-Mass., then head of the powerful House financial services committee, don't blame the White House for the failure of cramdown. But others certainly do. "Their behavior did not well serve the country," says Rep. Zoe Lofgren, D-Calif. It was "extremely disappointing."

When cramdown failed, Bair felt the complicated, weak incentives in HAMP doomed that program to failure: "I think Treasury wanted a press release. I think [Treasury Secretary] Tim Geithner and [then Obama economic advisor] Larry Summers wanted to be able to tell the president that they were doing something on loan mods."

"I got all dressed up"

Ramos' foreclosure made just as little sense to her as Wilshire's actions had. Suddenly, a company named Deutsche Bank was suing her. "This lawsuit that has been filed against me was very shocking since, I do not know who the plaintiffs are, or ever heard of them," she wrote in a handwritten note to the judge. "I have been paying thousands of dollars to another company 'Wilshire Credit Corp' (which never returns my calls, or acts upon paperwork they request from me)."

The full name of the plaintiff was "Deutsche Bank National Trust Company as Trustee for the MLMI Trust Series 2007-MLN1." For Ramos, it might as well have been another language. When Merrill Lynch assembled her security, it had hired Deutsche Bank, a massive German bank with a large U.S. presence, to be the trustee. The trustee's job was to channel payments from the servicer to the investors and act as the investors' representative. That meant Deutsche Bank appeared on foreclosure suits as the plaintiff, even though it was the servicer, Wilshire, that had chosen to foreclose and hired attorneys to pursue it.

Ramos tried to get an attorney but found they were either too expensive or said they couldn't help her. The Florida Bar ran a project to provide borrowers with free legal help, but it was only for people who hadn't been sued by their lenders yet, they informed her in a letter.

Fighting foreclosure alone has been the norm for homeowners during the crisis. Although many jurisdictions don't track the number of unrepresented homeowners, it's clearly the overwhelming majority of cases, according to a Brennan Center for Justice report. In New Jersey, for instance, 93 percent of foreclosure cases in 2010 had no attorney on record.

Ramos did her best to represent herself. One legal-services organization directed her to another county's courthouse, where a "self-help" area was set aside for borrowers who wanted to contest their foreclosures. No attorneys were there to help, but the court did provide information about the process and sample forms. She drove three hours and then carefully followed the model they had there for filing an "answer" to the motion to foreclose. In the three-page document she later filed with the court, she laid out her case in numbered paragraphs. She was a victim of predatory lending, she alleged. And since she'd learned during her long hours of research online that Mortgage Lenders Network had gone out of business shortly after her mortgage went through, she alleged there was no way that Deutsche Bank or anybody else could have recently acquired ownership of it.

For her court hearing, she bought a matching skirt and top at a secondhand store. "I got all dressed up, because I didn't want to look like a ragamuffin." She even donned heels, a throwback to her department store days. She arrived at the courthouse nervous but ready to plead her case. But her hearing had been rescheduled, she learned, though no one had told her. She didn't know what it meant. "I thought maybe they went through my records and evidence, and that's why it was canceled." At the very least, it meant she'd have a few more months in her home.

Ramos and her partner Dave Backus search for useful objects at the local dump and recycling center. (Paul Kiel/ProPublica)

Three and a half months later, she received a notice that her case was back on. Her hearing would be in 10 days. In response, she filed a five-page "Motion to Dismiss with Prejudice" and attached about 100 pages of everything she thought was relevant: news articles and court filings about Mortgage Lenders Network, letters from Wilshire and her emails to the governor and FBI about the misstatement of her income on her loan application. No one could mistake it for a filing by a lawyer, but she thought it was enough to show something was wrong. "I thought the court system would at least question it."

Her hearing, of which there is no transcript because the Citrus County courts don't transcribe foreclosure hearings, didn't last long. Ramos arrived with her neighbor, Dave Shea, but they say a court officer wouldn't let him in. She found herself in front of Citrus County Judge Carol Falvey, who was sitting by herself at the end of a long table. Wilshire's attorney was on the speakerphone. "I instantly felt intimidated," Ramos recalls.

At one point, Ramos objected that Deutsche Bank hadn't shown it owned the loan. The voice on the phone said the company had filed papers showing it had proper standing to sue. Ramos had never received them. She remembers the judge saying the attorneys should send her those documents. The voice agreed. Nevertheless, the judge signed a judgment of foreclosure.

Ramos' home would be sold. None of the accusations she'd made in her filings had been directly addressed, either in a written response from Wilshire's lawyers or in the judge's order. "It was like I'd never filed the paper," she says. The whole hearing had lasted a few minutes.

An address and a GPS

She emerged stunned and confused. She and Shea decided to see those documents themselves. The clerk's office was just downstairs, after all. They pulled her case file, a folder of about 200 pages, roughly half of which were Ramos' own submissions. What they found in the other documents was bewildering.

In October, Wilshire's lawyers had filed what they called the "Original Assignment of Mortgage." But the document purported to transfer her mortgage from a lender called Mortgage Lender's Acceptance Corp. to the Deutsche Bank trust. Her lender had been Mortgage Lenders Network. Who was Mortgage Lender's Acceptance Corp.?

The document gave an address in nearby Ocala. They decided to go check it out.

Following the directions from a GPS device, they found themselves at an office park. There was nothing like a Mortgage Lender's Acceptance Corp. to be found. Hoping to find the building's manager, they called the number on a sign advertising space for lease. "We get the guy who's been the manager of that building for five years," Shea says. He told them no business by that name had ever been there. Convinced they'd found still more fraud, the pair decided to go immediately to the authorities.

"We walked right in the front door of the state Attorney General's office," recalls Shea. Attorneys from the office spoke to them in the lobby for about 20 minutes. "I was hoping they would stop the fraud," says Ramos, but instead they asked her to send a written complaint. She says she did so but never heard back. Theresa Edwards, a former assistant attorney general in Florida, says the office was inundated with such complaints.

The assignment is unquestionably an error. Mortgage Lender's Acceptance Corp., to start with, was not her lender and never had any connection to her actual lender, Mortgage Lenders Network. The assignment even has an error in how the wrong company's name is written; the apostrophe is misplaced, presenting the name as Lender's instead ofLenders'. A company called Mortgage Lenders' Acceptance Corp. was once active in Florida, according to an incorporation filing, but not since the late 1990s.

Two parties are responsible for the mistake. The first is Wilshire, which employed the woman who signed the document. The other is the law firm working on Wilshire's behalf, Smith, Hiatt & Diaz, a large Florida firm that handles thousands of foreclosures a year — what critics would call a foreclosure mill. Generally, the servicer's attorneys prepare the assignments and send them to the servicer to be executed. Whoever actually entered in the wrong lender, Wilshire's employee signed off on it, and Smith, Hiatt & Diaz filed it with the court. Attorneys at Smith, Hiatt & Diaz did not respond to multiple calls and emails requesting comment.

That's who's responsible, narrowly defined. The real culprit, as with almost all servicing problems, is the bottom line. To save money, servicers usually do not document ownership of a mortgage until it's necessary to foreclose. Instead, servicers keep on file blanket authorizations for their employees to sign on behalf of the lenders whose loans they handle. As a result, a single servicing employee might sign hundreds of documents in a day on behalf of as many as a dozen or more different lenders. Often, that low-level employee will sign as a vice president of this or that bank.

The process has produced laughable errors, transferring the mortgage to "Bogus Assignee" or dating a document "9/9/9999." "People just aren't paying attention," says Edwards, the former Florida assistant attorney general who now defends borrowers from foreclosure. "They're running them through so quickly they make mistakes."

While working with the attorney general's office in 2010, Edwards and a colleague cataloged examples of the industry's documentation practices in a presentation for county officials titled "Unfair, Deceptive and Unconscionable Acts in Foreclosure Cases."*

At some servicers or companies working on their behalf, employees forged the signatures of other employees. The most famous of these is "Linda Green," an actual employee of DocX, a company that specialized in document production. Her name, with a signature obviously penned by many different hands, adorns tens of thousands of documents filed across the U.S. Green and other former employees of DocX, which was shut down in 2010, told 60 Minutes that management instructed them to sign on Green's behalf. Last year, one of the servicers that had hired DocX sued the company in a Texas court, alleging that more than 30,000 documents had been improperly executed. The servicer, American Home Mortgage Servicing, claimed it had been ignorant of what DocX termed "surrogate signing," and is suing for damages. Lender Processing Services, DocX's parent company, does not dispute that its employees were forging signatures but said the company had gone back to fix the affected assignments and is contesting the suit.

While servicers say employees shouldn't sign another person's name, the servicers insist there's nothing wrong with their employees signing on behalf of other companies as long as proper authorization has been granted.

But in some cases, servicers have filed documents without any authorization. Internal documents obtained by ProPublica show that the nation's fifth-largest servicer, GMAC Mortgage, did just that. GMAC, a subsidiary of Ally Financial, wanted to pursue foreclosure against a New York homeowner, but the original lender had gone out of business.

"The problem is we do not have signing authority," Jeffrey Stephan, the head of GMAC's "Document Execution" team, wrote in an email. Stephan went ahead and signed a document purporting to be an officer of the defunct lender anyway. A GMAC spokeswoman acknowledged Stephan didn't have authority to sign the document and said the company was planning to pursue foreclosure on the loan after it resolved the problem.

The MERS mirage

What is shocking about Ramos' case — the false transfer of her mortgage from a defunct company that had never been connected to her loan — is that it is anything but unusual. Hers and thousands of similar cases could be written off as errors, shoddy and outrageous perhaps but mostly unintentional. But alongside those errors was something else entirely: The mortgage servicing industry deliberately avoided publicly documenting ownership of loans. Indeed, the industry had created a sophisticated strategy to avoid filing legal documentation of who actually owns a mortgage.

The strategy involves a kind of shell company, one that exists to avoid government fees and allow gigantic financial institutions to toss mortgages to each other as easily as if they were baseballs. It is a system that takes the once public and legal record of ownership — who the homeowner owes money to — and embeds it inside a private company.

The document that transferred Ramos' mortgage to Deutsche Bank is signed by a woman purporting to be an "Assistant Secretary" of "Mortgage Electronic Registration Systems, Inc. as nominee for Mortgage Lender's Acceptance Corp.," a seemingly hopeless trail of abstractions. But Mortgage Electronic Registration Systems, or MERS, is an industry creation. When lenders record a mortgage or assignment, they have to pay a fee to a county office. To avoid billions in fees and make it easier to transfer mortgages, the industry launched MERS in the 1990s.

MERS does two things. Its computer system keeps track of loans. But more important, MERS poses as the true lender in public records. If a mortgage states that MERS is the lender's "nominee," then MERS can take its place — at least on paper. In the county clerk's office, the mortgage is registered not to Mortgage Lenders Network or Merrill Lynch or Deutsche Bank or any other institution that actually lends money to a homeowner, but to MERS. And any changes in real ownership of the mortgage, such as when Mortgage Lenders Network sold Ramos' mortgage to Merrill Lynch, is recorded only inside MERS, not in public records. With MERS, no matter how many times a loan is bought and sold, there's usually no need to file anything else or pay any extra fees — until it's time to foreclose.

The system currently contains roughly half of the nation's active mortgages, or about 30 million.

Even though MERS has only a few dozen employees, the company has authorized at least 8,000 people at hundreds of other companies — typically servicers but also law firms and other companies — to sign as officers of the company. That's how Ramos' assignment came to be signed by a Wilshire employee in Oregon purporting to be an "Assistant Secretary" of Virginia-based MERS.

MERS spokeswoman Janis Smith said the Wilshire employee had been properly appointed as a MERS officer.

Maybe, but a number of municipalities have sued MERS, seeking to recoup lost fees and charging the company with fraud. The latest and biggest suit, in early February, came from the New York attorney general, who charged MERS and three major banks, including Bank of America, of widespread document fraud. New York's suit charges that the industry's use of MERS to facilitate foreclosures has led to filing "false and deceptive" documents.

MERS says the system is legal and that it will fight the suit.

The involvement of MERS explains why Ramos and Shea didn't find any lender at the office park. The address listed for Ramos' lender — the no-longer-operating-in-Florida Mortgage Lenders' Acceptance Corp. — was actually MERS' registered Florida address at the time. Maintained by a separate corporate services company, the address existed merely to satisfy state law and receive mail. In trying to find an actual lender at the address, Ramos had been chasing shadows.

"You feel powerless to help"

On the morning of April 13, 2009, Sheila Ramos waited at home to hear whether her last chance to avoid foreclosure had been successful. This time, she had her own lawyer, who was at that moment arguing her case to the judge. Ramos was hopeful. After all, how could a judge give away her home on the basis of the phony paperwork she had uncovered?

That couldn't stand. Finally, they'd have to deal with her. They'd have to acknowledge her loan was fraudulent in the first place. After a year of fighting and complaining to every authority she could think of, she would finally be heard.

Just finding an attorney to represent her had been an ordeal. One she'd contacted told her he couldn't help but suggested Janet Varnell, a prominent consumer advocate attorney in central Florida, so Ramos gave her a try.

Varnell was hesitant. An experienced litigator, she'd never handled a foreclosure case. The Florida Bar, however, had been pushing attorneys to take cases no matter their experience in the area because of the overwhelming need in the state. Legal aid organizations couldn't keep up. Varnell, who runs a practice with her husband, felt a responsibility to try it.

"Despite never having done a day of foreclosure defense in my life, I knew better than the average attorney what to do," she says.

And Ramos had a strong case, Varnell thought. Not only was Ramos a victim of predatory lending, she thought, but the documents used to foreclose on her were clearly flawed. "There's someone on every corner in Florida who's in desperate need of help, so you don't just go running around offering help to people who don't have substantial claims," she says.

Varnell not only took the case for free but paid the $50 fee to reopen the case. About two weeks before Ramos' home was scheduled to be sold, Varnell submitted a motion to cancel the sale, overturn the judgment and dismiss the foreclosure suit altogether.

At the center of her argument was the faulty assignment. Typical of the servicer's last-minute rush to collect the documents necessary to foreclose, the assignment was actually dated a day after Smith, Hiatt & Diaz, Wilshire's law firm, filed suit against Ramos. The original complaint had asserted that "Deutsche Bank National Trust Company as Trustee for the MLMI Trust Series 2007-MLN1" was the holder of the note and mortgage, but offered no documentation to support that. Instead, all that had been attached was a copy of the note and mortgage made out to Mortgage Lenders Network, the original lender. The assignment, dated the next day and filed months later, couldn't fix that problem, she argued. It only made matters worse that the assignment was itself obviously flawed, confusing things further by referring to the wrong lender.

The early signs for Ramos were good. Smith, Hiatt & Diaz responded to the motion by immediately moving to cancel the upcoming sale. A hearing was quickly scheduled. Varnell would have Judge Falvey's ear for a 15-minute phone call.

Falvey wasn't impressed. Again, because the county does not transcribe foreclosure hearings, there's no transcript, but Varnell remembers the judge being dismissive of the flaws in the mortgage's documents. The foreclosing party appeared to have the note and mortgage, and that was good enough for her.

When asked about the ruling, Falvey's assistant said the judge doesn't comment on individual cases.

Ramos was crushed, and so was Varnell. "Frankly, it came as a shock," the lawyer recalls. "I remember crying when I knew the judge was not going to give us our day in court ... crying more for myself because you feel powerless to help."

In the wake of the legal defeat, Varnell struck a deal with the attorney from Smith, Hiatt & Diaz: If Varnell did not appeal Falvey's ruling, Wilshire would indefinitely postpone the foreclose sale and evaluate Ramos for a modification.

Knowing what she knows now, Varnell wrestles with this decision. It was a kind of capitulation but a realistic one, she thinks. At the time, in early 2009, few Florida state court decisions clearly established that the lender needed to clearly establish ownership of the note and mortgage in order to foreclose. "The law was not really well advanced at the time," she says.

Since then, a number of similar cases have made their way to the appellate level. In late 2011, Florida's 4th District Court of Appeal overturned two district decisions because, as in Ramos' case, the lender hadn't executed an assignment before the complaint.

"If I had been in this situation today," says Varnell, "I probably would have gone on and filed the appeal, and I feel I would have won."

Since losing Ramos' case, Varnell has represented more than a dozen other homeowners and had much more success, even getting some of the foreclosure suits thrown out.

From the perspective of the mortgage industry, borrowers are just finding a "technical legal argument to get out of paying your mortgage" by seizing on flawed documents, said Tom Deutsch, executive director of the American Securitization Forum, which counts the country's biggest banks among its members. When mortgages like Ramos' were sold to Wall Street banks like Merrill Lynch, agreements clearly laid out the transfers, he says, and there's no "role for the court there to look any farther than that clear chain of title."

Many judges haven't agreed, sometimes dealing the banks high-profile defeats, as the Massachusetts Supreme Court did in early 2011.